“The postponement of the Georgia factory’s opening allows Rivian to recalibrate its expansion strategy in response to the current economic environment”

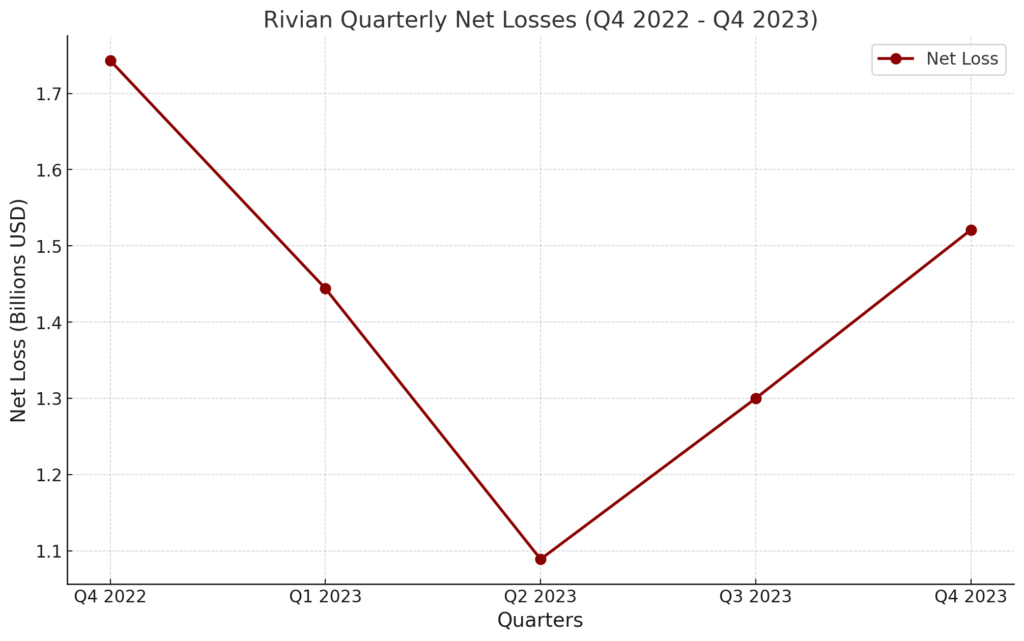

Graph Details

The graph illustrates Rivian Automotive’s quarterly net losses over five quarters, from Q4 2022 to Q4 2023. It reveals a trend of fluctuating losses, with a notable decrease in losses from Q4 2022 to Q1 2023, followed by a continued decline into Q2 2023. However, there’s a slight increase in losses in Q3 2023 before they rise again in Q4 2023. This pattern reflects Rivian’s ongoing efforts to scale production, manage costs, and navigate the financial complexities of the electric vehicle market. While the company is making progress, as indicated by the overall reduction in losses from Q4 2022, the graph underscores the challenges Rivian faces on its path toward achieving profitability.

Introduction

Rivian Automotive, Inc., an innovative player in the electric vehicle (EV) industry, has been making strides in its journey toward financial stability and market expansion. Despite facing significant losses, the company’s operational strategies and market positioning signal a dedicated effort toward scalability and growth.

Rivian’s Place In The EV Industry

Rivian stands out with its innovative product lineup, particularly the R1T and R1S models, underpinned by advanced technology and strategic partnerships, notably with Amazon and access to Tesla’s Supercharger network. These initiatives, alongside a growing charging infrastructure, position Rivian strongly in the rapidly evolving EV market. However, the company’s financial performance shows a need for careful navigation through challenges of production scaling, capital acquisition, and market competition (Yahoo Finance) (Kavout).

Financial Overview

In 2023, Rivian’s financial data revealed a path of gradual improvement with a reduction in losses and controlled operating expenses. The company reported a net loss of $1.521 billion in Q4 2023, a decrease from the previous year. The adjusted EBITDA loss for the same period also showed improvement. Despite these losses, Rivian’s liquidity position remains strong, with significant cash reserves to support ongoing operations and growth initiatives (Rivian) (MarketBeat).

Operational Efficiency

Rivian’s operational focus has been on ramping up production and delivering a growing number of vehicles, evident in its significant increase in production and delivery figures for 2023. The company’s emphasis on technological enhancements, like the latest software updates for its vehicles, demonstrates a commitment to improving customer experience and vehicle functionality, crucial for maintaining competitiveness and driving consumer adoption (Kavout).

Growth Strategies

Rivian’s growth trajectory is marked by its ambitions in the EV market, underscored by production increases and market expansion efforts. The company’s proactive approach to scaling operations and its strategic positioning in California, a key EV market, showcase its potential to capitalize on the sector’s growth. However, Rivian’s journey towards profitability is punctuated with the need for continuous innovation, strategic market positioning, and navigating financial challenges (Kavout).

Challenges and Risks: Navigating Factory Delays and Interest Rate Slowdown

Rivian, while navigating the competitive electric vehicle (EV) landscape, confronts significant challenges, particularly with its recent decision to delay the opening of its new manufacturing plant in Georgia. This delay is a strategic move amid a broader economic context influenced by fluctuating interest rates and the need for careful financial and operational planning.

The postponement of the Georgia factory’s opening allows Rivian to recalibrate its expansion strategy in response to the current economic environment, where interest rate changes are impacting the automotive industry, especially the EV sector. Slowing down the pace of new investments and focusing on enhancing the production capabilities at its existing Normal, Illinois, plant for the upcoming R2 model could be a prudent approach to manage costs and optimize resources during this period.

This strategy may offer Rivian several advantages in managing the interest rate-induced slowdown. By concentrating on the Normal plant’s tooling for the R2 production, Rivian can potentially improve its production efficiency and product quality, which are critical for maintaining competitiveness and consumer trust in a market that is increasingly sensitive to interest rate fluctuations.

However, this approach is not without risks. Delaying the Georgia plant’s opening could impact Rivian’s long-term growth plans and its ability to meet future demand increases, especially as the EV market continues to expand. Moreover, the reliance on a single manufacturing facility in the interim increases vulnerability to any unforeseen operational hiccups that could disrupt production.

In addition, Rivian’s financial sustainability is under scrutiny, with the company’s significant reliance on capital markets for funding. In a time when the EV sector is seeing intensified competition, Rivian’s ability to secure necessary funding and manage its capital expenditure efficiently while navigating these delays will be crucial for its continued growth and market positioning.

In essence, Rivian’s strategy to delay its Georgia factory opening, while focusing on enhancing its existing facilities amid an interest rate-induced economic slowdown, reflects a cautious approach to scaling and financial management. This decision underscores the company’s responsiveness to the broader economic landscape but also highlights the inherent challenges and risks in managing production scale, financial stability, and strategic growth in the dynamic EV industry.

Conclusion

Rivian’s path to profitability remains a closely watched aspect of its financial journey. While the company has made significant strides in scaling up its production and deliveries, as evidenced by its substantial increase in vehicle production and deliveries in 2023, it is still facing considerable financial losses. In the fourth quarter of 2023, Rivian reported a net loss of $1.521 billion, although this was an improvement compared to the previous year’s figures. The company’s adjusted EBITDA for the same quarter also showed an improvement, signaling a potential trajectory towards reducing losses over time (Rivian).

However, Rivian is still in a phase where it is ramping up production and investment to capture market share in the competitive EV industry. The company’s earnings report for the last quarter of 2023 indicated a loss per share of $1.58, which, while better than expected, still underscores the challenges Rivian faces in achieving profitability. The financial community’s consensus estimates project ongoing losses per share for the current and next year, although there is an expectation of improvement (MarketBeat).

Given these factors, while Rivian is making progress in its operational and financial performance, it is not yet profitable and is navigating through a critical period of investment and growth. The company’s future profitability will likely depend on its ability to continue increasing production and sales, improve operational efficiencies, and manage its capital and expenses strategically in the evolving EV market landscape.